Do you need life insurance for a mortgage

No. Life insurance is not a legal requirement for a mortgage in the UK, and no lender can refuse you one for going without it. The only cover lenders insist on is buildings insurance. But if someone shares your mortgage or depends on your income, it is usually a smart move.

Get my quoteThe short answer

You do not need life insurance to get a mortgage in the UK. There is no law, no Financial Conduct Authority rule and no lender code that makes it compulsory, and a lender cannot turn you down simply because you decline it.

The one cover lenders do insist on is buildings insurance, because the property is their security. Life insurance is different. It protects your family, not the bricks. It is optional, but if a partner shares your mortgage or your income helps pay it, it is usually money well spent.

Is it a legal requirement

No. There is no UK law, no Financial Conduct Authority rule and no lender regulation that says you must hold life insurance to be granted a residential mortgage. A lender cannot refuse your application solely because you have not taken out a policy. If an adviser tells you cover is compulsory and will not proceed without it, that is not correct.

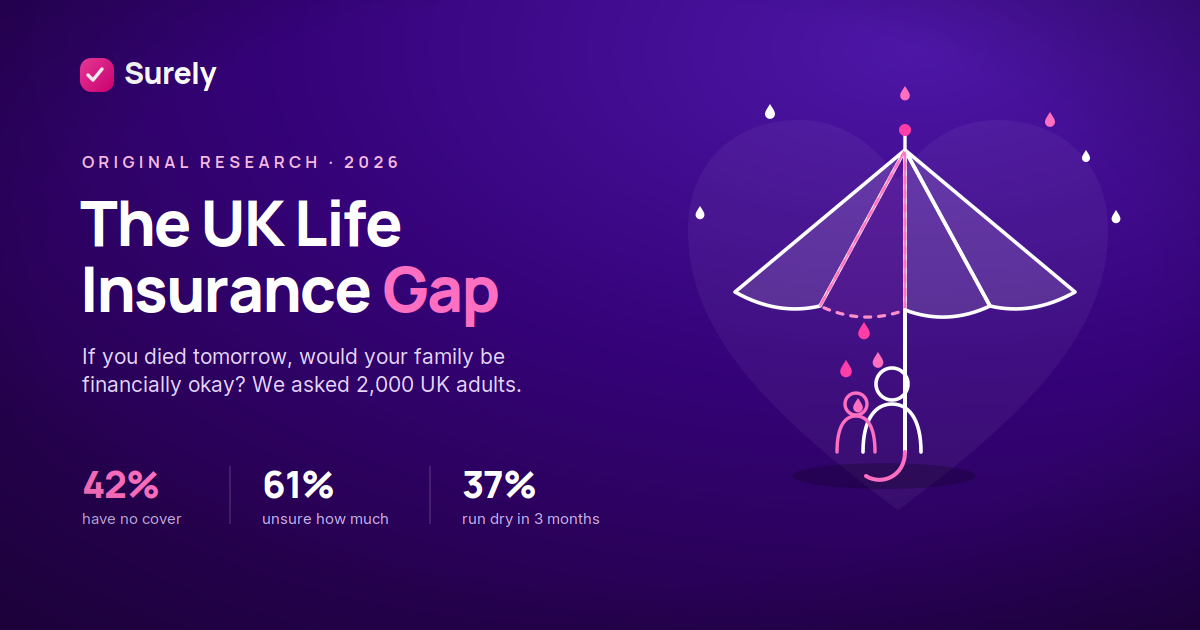

The belief is surprisingly common. In a 2026 survey of 2,000 UK adults, 31 percent thought a life policy was required for a mortgage, rising to 40 percent among younger adults.1 The myth survives partly because lenders and brokers often sell cover alongside the mortgage, so it can feel like part of the deal. It is not.

The cover lenders do need

There is one insurance lenders insist on, and it is not life insurance. It is buildings insurance, which pays to repair or rebuild your home after damage such as fire or flood. Lenders require it from the day you exchange contracts because the property is the security for their loan, and they will hold back the money on completion day if it is not in place.

Even this is not set by law. It comes from the lender’s own loan terms. So the simple rule is this. Buildings insurance protects the bricks for the lender. Life insurance protects your family. Only the first is a condition of the mortgage.

What happens to your mortgage if you die

A mortgage does not disappear when you die. The debt becomes part of your estate, and the lender still needs paying. If your household cannot keep up the repayments from what is left, the home may have to be sold, or in the worst case repossessed, to clear what is owed.

This matters most with a joint mortgage. If one of you dies, the survivor usually becomes responsible for the whole repayment on their own, often on a single income. That is the gap life insurance is designed to close. A payout can clear the mortgage so the people you leave behind can stay in their home.

When you should still get it

It is optional, so the honest test is whether anyone would be left struggling without your income. You should seriously consider cover if any of these apply.

- You have a family who depend on your income, such as a partner or children.

- You have a joint mortgage, where one death would leave the other with the full repayment.

- You have an interest only mortgage, where none of the loan is being paid off, so the whole balance is still owed at the end.

You may not need it if you are single, have no dependants and no one shares the loan, because the property could simply be sold to clear the debt. Even then, some people still want cover to pay for a funeral or to leave the home to someone. If you are weighing it up more broadly, our guide on whether you need cover at all goes wider than the mortgage.

“The myth that you must have it for a mortgage does real harm. People either buy in a panic at the lender’s desk without comparing, or they assume it is forced on them and resent it. Neither is right. Nobody can make you buy it. Decide it on one thing alone, whether your family could keep the home without your income, then shop around calmly.”

The cover that fits a mortgage

Two types of cover are built for mortgages, and which one fits depends on your mortgage.

Decreasing term cover, often sold as mortgage life insurance, has a payout that falls over time, roughly in line with a repayment mortgage balance. It is the cheapest option and suits a repayment mortgage, where the amount you owe shrinks each year.

Level term cover keeps the same payout the whole way through. It suits an interest only mortgage, where the full balance is owed until the end, or anyone who wants to leave extra on top of clearing the loan. Whichever you choose, match the length of the policy to the years left on your mortgage.

How much it costs

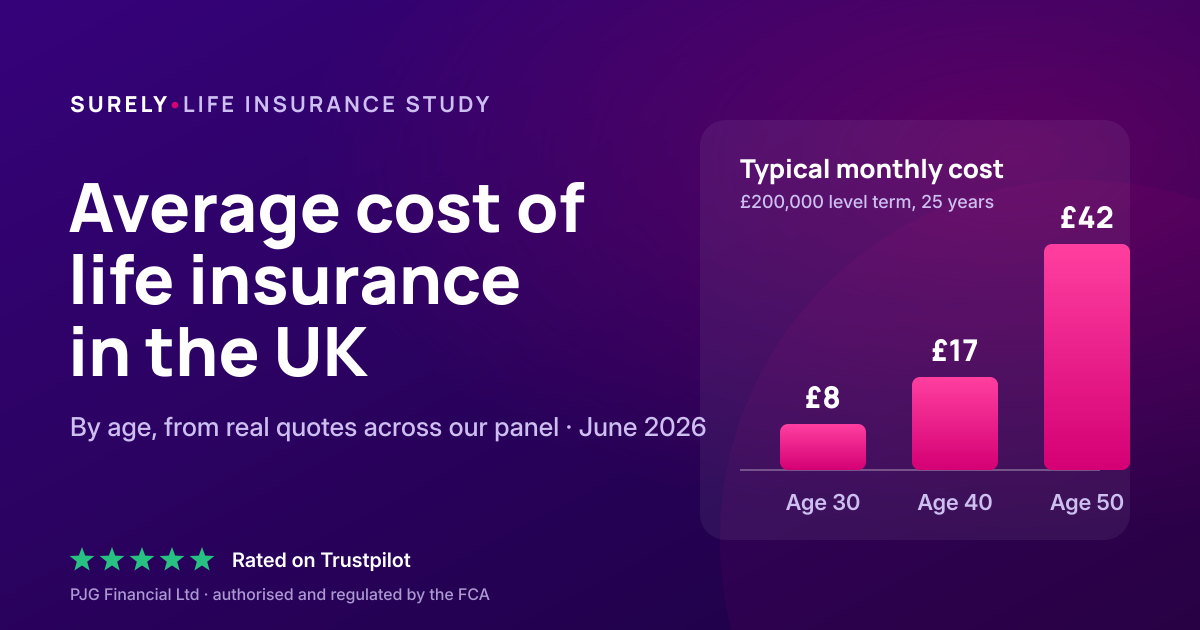

Cover is cheap next to the size of the debt. Recent averages put decreasing term cover at about 17 pounds a month and level term at about 25 pounds a month.3 Your own price depends on your age, health, the amount and length of cover and the insurer, so buying while you are younger and healthier locks in a lower rate. Our guide to how much life insurance costs breaks the figures down further.

It is worth knowing two related covers exist. Income protection pays you a monthly income if illness or injury stops you working, which helps keep the mortgage paid while you are alive. Critical illness cover pays a lump sum if you are diagnosed with a serious condition. Both can sit alongside life cover, and neither is required for a mortgage.

How much cover you need

As a starting point, enough to clear the outstanding mortgage balance, so your family is not left with the loan. For a repayment mortgage, decreasing cover that tracks the balance does this neatly. For an interest only mortgage, you need level cover for the full amount.

Many people choose to add a buffer on top, so the payout covers more than the bricks. Lost income, childcare and everyday living costs do not stop when you die, so cover set only at the mortgage balance can leave a family with the home but no money to run it. A common approach is the mortgage plus a few years of income.

Single, joint or two policies

Couples with a shared mortgage often take joint life cover, which pays out once, on the first death, then ends. It is simple and usually a little cheaper than two policies. The trade off is that it pays only once, and the survivor is left with no cover.

Two single policies can each pay out, so a couple could in theory receive two payouts, and the survivor keeps their own cover afterwards. The cost is often only modestly higher. Which suits you depends on your budget and what you want to leave behind.

Should you put it in trust

For mortgage cover it is often worth writing the policy in trust, a legal arrangement that holds the payout outside your estate. It means the money usually reaches your family faster, without waiting for probate, and is kept clear of inheritance tax. Setting up a trust is normally free when you take out the policy.

Tax treatment depends on your personal circumstances and on current law, which can change. A trust is a legal arrangement, so consider taking advice for anything beyond the straightforward.

Common questions

Is life insurance required for a mortgage in the UK?

No. It is not a legal or regulatory requirement, and no lender can refuse you a mortgage solely because you decline it. The only cover lenders insist on is buildings insurance.

Can a lender refuse me a mortgage if I do not have life insurance?

Not for that reason alone. Affordability is assessed on your income, outgoings and credit history, not on whether you hold a life policy. A lender can, however, require buildings insurance as a condition of the loan.

What insurance do I actually need for a mortgage?

Buildings insurance, in place from exchange of contracts, because the property is the lender’s security. Contents, life, critical illness and income protection are all optional.

What happens to my mortgage if I die?

The debt passes to your estate and the lender still needs paying. If the repayments cannot be met, the home may have to be sold. On a joint mortgage, the survivor usually becomes responsible for the whole repayment.

Should I choose decreasing or level cover for a mortgage?

Decreasing cover suits a repayment mortgage, because it falls roughly in line with the balance and costs less. Level cover suits an interest only mortgage, or anyone who wants to leave extra beyond clearing the loan.

Do I need it if I am single with no dependants?

Usually not as a priority. With no one sharing the loan, the property could be sold to clear the debt. You might still want cover to pay for a funeral or to leave the home to someone.

The mortgage cover question in numbers

A summary of the figures behind this guide.

| The picture in numbers | Figure |

|---|---|

| UK adults who wrongly think it is required for a mortgage | 31% |

| That figure among younger adults | 40% |

| Insurance lenders actually require | Buildings insurance |

| Average UK house price, April 2026 | £270,080 |

| Typical cost to cover a repayment mortgage | About £17 a month |

| Adults who held life insurance in 2024 | 28% |

| Life insurance claims paid in 2024 | 96.5% |

Surely analysis of the 2025 Life Insurance Index, FCA Financial Lives 2024, ONS UK House Price Index, myTribe 2026 pricing survey and ABI protection claims 2024.12534

Deciding what is right for you

Life insurance is not something a mortgage forces on you. It is a choice, and a sensible one for most people who share a mortgage or have a family relying on their income. Work out whether your household could keep the home without you, cover at least the outstanding balance, match the cover type to your mortgage, and compare a few insurers rather than signing whatever is put in front of you at the lender’s desk.

Cover, price and eligibility depend on your personal circumstances, including your age, health, occupation and smoker status, and on insurer terms. Surely is operated by PJG Financial Ltd, which is authorised and regulated by the Financial Conduct Authority, FRN 919697.

How we researched this guide

We write our guides from named, public UK sources and cross check the figures rather than rely on a single site. Where we say “Surely analysis”, it means we have compiled and compared published data, not produced the raw figures ourselves.

The data on this page draws on:

- The 2025 Life Insurance Index, commissioned by UK-lifeinsurance.com, a survey of 2,000 UK adults, for the misconception figures.

- The Financial Conduct Authority, Financial Lives 2024 survey, for the share of adults holding life insurance.

- The FCA Mortgages and Home Finance: Conduct of Business sourcebook, for the regulatory position on what a mortgage requires.

- myTribe Life Insurance Pricing Survey 2026, for average monthly premiums.

- ABI protection claims data 2024, and the ONS UK House Price Index, for claims paid and the average house price.

Cost figures are illustrative averages, not quotes. Your own price will depend on your age, health, the cover you choose and the insurer.

Surely compares cover from a selected panel of UK insurers and protection providers, not the whole of the market. Surely may receive a commission from the provider you take out cover with, which does not affect the price you pay.

Written and reviewed by Paul Gillooly, Founder of Surely. Last reviewed June 2026.

Sources

- 2025 Life Insurance Index, commissioned by UK-lifeinsurance.com, survey of 2,000 UK adults (Censuswide). 31% believe life insurance is required for a mortgage, rising to 40% of younger adults and 44% in Northern Ireland.

- Financial Conduct Authority, Financial Lives 2024 survey. 28% of adults held life insurance in 2024, with above average declines among mortgage holders. fca.org.uk

- myTribe Life Insurance Pricing Survey 2026. Average monthly premiums: decreasing term £16.58, level term £25.05.

- Association of British Insurers, protection claims data 2024, published July 2025. 96.5% of new life insurance claims paid; £5.32 billion in individual protection claims. abi.org.uk

- ONS and HM Land Registry, UK House Price Index, April 2026. Average UK house price £270,080. gov.uk

- Financial Conduct Authority Handbook, Mortgages and Home Finance: Conduct of Business sourcebook (MCOB). Contains no requirement to hold life insurance for a residential mortgage.