Compare the best UK life insurance

The best policy is the one that fits you, at a fair price, from an insurer that pays claims. Here is how the major UK insurers compare on payout, what to look for in a policy, and what cover typically costs.

Get my quoteSurely helps you compare and get quotes online; we do not give advice ourselves; where advice is appropriate, a qualified protection adviser from our panel partners may contact you.

What does best actually mean?

There is no single best life insurer for everyone. The best policy is the one that covers what your family needs, at a fair price, from an insurer with a strong record of paying claims. The cheapest quote is not automatically the best, and the most expensive is not automatically the safest.

The good news is that the major UK insurers all pay close to every valid claim, so reliability is rarely the deciding factor. The real differences sit in price and terms, which is exactly where comparing pays off.

What best really means

It is tempting to look for a single winner, but life insurance does not work that way. The insurer that offers you the lowest price may offer someone else a higher one, because each insurer weighs your age, health and lifestyle in its own way. So best is personal. Three things decide it.

- Payout reliability. Whether the insurer pays claims. Across the major insurers this is consistently high, but it is still worth checking.

- Price. The monthly premium for the exact cover you want. This is where insurers differ most.

- Terms and features. The definitions and extras that fit your situation, such as guaranteed premiums or cover that keeps pace with inflation.

Get all three right for your circumstances and you have found your best policy. The rest of this page shows you how, starting with the figures that matter most.

How reliably claims are paid

A low price only matters if the policy pays out when it is needed, so this is where best really starts. The reassuring news is that payout rates across the UK are high.

In 2024, UK insurers paid a record £8 billion in protection claims, the equivalent of around £21.9 million every day.1 Across individual protection, 97.9% of claims were paid, a level that has held for a decade, and the average life insurance payout was £79,703.1 The small share declined is mostly down to non disclosure, which is within your control: answer every question honestly when you apply.

What the major insurers paid in 2024

Individual insurers publish their own claims figures each year. The chart and table below show what some of the largest UK life insurers reported for 2024.

| Insurer | Claims paid in 2024 | Proportion paid |

|---|---|---|

| Aviva | £862.1m in life and terminal illness claims2 | 98.8% |

| Royal London | £751m across all protection claims3 | 98.7% of all claims |

| Legal & General | £583m in life claims4 | around 97% |

| LV= | £137m across individual protection5 | 95% of all individual claims |

| Industry (ABI and GRiD) | £8bn across group and individual protection1 | 97.9% of individual claims |

Figures are as published by each insurer or the ABI for 2024. The scope differs, so some report life only, some life and terminal illness, and some all protection. Treat them as a guide to reliability rather than a like for like ranking.

The takeaway is that payout reliability is high across the board. That means the real differences between insurers tend to sit in price and terms, which is where comparing earns its keep.

How much the same cover varies

For exactly the same cover, the same term and the same person, insurers can quote prices that differ by 20% to 40%.6 Each insurer prices risk in its own way, weighs your age, health and lifestyle differently, and runs its own offers, so there is no reliable shortcut to predict who will be cheapest for you. Comparing a few quotes for your exact cover is the only way to find your best price.

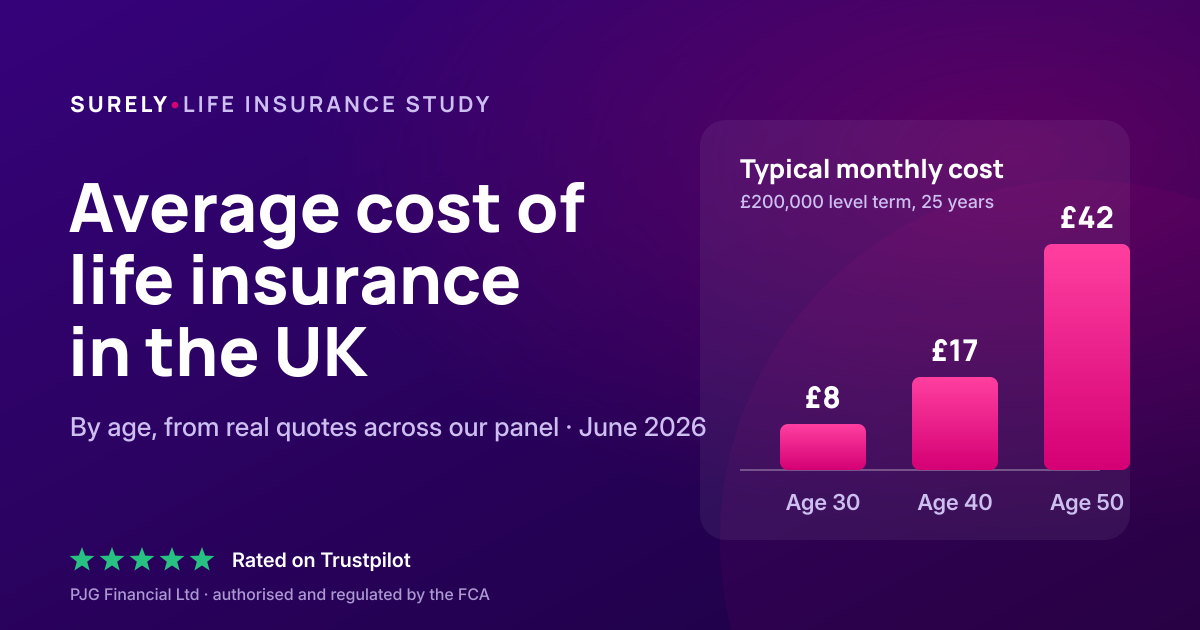

To set your expectations before you compare, here is a guide to typical monthly premiums for a healthy applicant. Figures are Surely analysis and illustrative, not quotes.6

| Age | Illustrative monthly premium |

|---|---|

| 30 | £11 |

| 40 | £23 |

| 50 | £55 |

| 60 | £130 |

Premiums roughly double every decade. Smoking roughly doubles the price, and decreasing term is typically 25% to 40% cheaper than level term. These are starting points, so always compare for your exact details.

What to compare beyond price

Once price and payout are sorted, the terms decide whether a policy genuinely fits. These are the features worth checking.

| Feature | Why it matters |

|---|---|

| Terminal illness cover | Usually included. Pays out early if you are diagnosed with a terminal illness, typically with under 12 months to live. |

| Guaranteed premiums | The price is fixed for the whole term. Reviewable premiums can be cheaper at first but may rise later. |

| Waiver of premium | Covers your premiums if illness or injury stops you working, so the policy stays in force. |

| Indexation | Lets your cover rise with inflation each year, so its real value does not fade over a long term. |

| Single or joint | Two single policies pay out twice. A joint policy pays once and ends, which is usually cheaper but covers one claim. |

| Written in trust | Speeds up payment to your family and can keep the payout outside your estate for inheritance tax. |

| Added support | Many policies include extras such as virtual GP access or bereavement support at no extra cost. |

Not every feature suits every person. A young family on a tight budget may prioritise a low guaranteed premium, while someone protecting a 30 year mortgage may value indexation more.

How to compare well

- Decide your cover first. Settle on the amount and term you need before you look at prices, so you compare like for like.

- Get quotes for that exact cover. Compare the same amount, term and cover type across insurers, not different policies.

- Weigh price against terms. Payout records are high across the major insurers, so let price and the right definitions guide you.

- Check the premium type. Guaranteed premiums avoid surprises later. Make sure you know which you are buying.

- Consider help for complex health. If you have a health condition, a panel that includes specialists can find better terms.

- Never cancel old cover early. Keep any existing policy in force until the new one has started.

“People ask me which insurer is best, and the honest answer is that it depends on you. The big names all pay out on close to every valid claim, so reliability is rarely the thing that separates them. What separates them is price, where the same cover can cost a third more from one insurer than another, and the terms. Get the cover amount right, then compare on those.”

Frequently asked questions

Which insurer is the best?

There is no single best insurer for everyone. The best policy is the one that fits your needs at a fair price from an insurer that pays claims. Because the major insurers all pay close to every valid claim, the decision usually comes down to price and terms, which is why comparing a few for your exact cover matters.

Do all insurers actually pay out?

Payout rates are high across the UK. Around 97.9% of individual protection claims were paid in 2024, and major insurers reported life and protection claims paid rates close to 99%, including Aviva at 98.8% and Royal London at 98.7%.123 The small share declined is mostly down to non disclosure, so being honest on your application is what keeps a claim valid.

Why do prices vary so much for the same cover?

Each insurer prices risk in its own way, weighs your age, health and lifestyle differently, and runs its own offers. That is why the same person can be quoted prices that differ by 20% to 40% for identical cover.6

Is the cheapest policy a good idea?

Often, yes, as long as the definitions fit your needs. Because payout records are strong across the major insurers, a low price with the right cover type and a guaranteed premium is usually a sound choice. Check the terms rather than the headline price alone.

Should I keep my current policy or switch?

It can be worth comparing, since prices and your circumstances change. Be careful though. A new policy will be priced on your current age and health, you may lose a good guaranteed rate, and you should never cancel existing cover until the new policy is in force.

Does Surely give advice?

Surely helps you compare and get quotes online; we do not give advice ourselves; where advice is appropriate, a qualified protection adviser from our panel partners may contact you.

For impartial money guidance you can use MoneyHelper, the government backed service.

Getting started

Decide on the cover amount and term that suit your family, then compare quotes for that exact cover across a few insurers. Since payout records are strong across the major names, weigh the price against the terms, check whether the premium is guaranteed, and consider writing the policy in trust. Answer every question honestly so your cover pays when it is needed.

Insurer claims figures on this page are as published by each insurer or the ABI for 2024 and cover different product mixes, so they are a guide to reliability, not a like for like ranking. Pricing figures are Surely analysis of typical UK prices for a healthy applicant and are illustrative, not quotes. Your actual price depends on your full details and the insurer, and is confirmed only when you apply. Surely helps you compare insurance and does not provide regulated financial advice.

How We Researched This Guide

We write our guides from named, public UK sources and cross check the figures rather than rely on a single site. The data on this page draws on:

- Association of British Insurers and Group Risk Development, 2024, for the £8 billion total, the 97.9% individual claims paid rate and the average life payout.

- The published 2024 claims reports of Aviva, Royal London, Legal & General and LV=, for their individual payout figures.

- Surely analysis of typical UK term life prices for a healthy applicant, for the average prices and the 20% to 40% variation between insurers.

- Financial Conduct Authority Pure Protection Market Study, January 2026, for market context.

We name insurers only alongside their own published claims figures, with sources. We do not attach prices to named insurers, because real per insurer prices are not publicly referenceable, so pricing here is aggregate Surely analysis. Claims figures cover different product mixes, so they guide reliability rather than rank insurers. Surely helps you compare and get quotes online; we do not give advice ourselves; where advice is appropriate, a qualified protection adviser from our panel partners may contact you.

Written and reviewed by Paul Gillooly, Founder of Surely. Last reviewed June 2026.

Sources

- Association of British Insurers and Group Risk Development, “Record £8bn paid out in vital protection claims during 2024”, July 2025: record £8 billion paid; 97.9% of individual protection claims paid; average life insurance payout £79,703.

- Aviva, 2024 claims data: 98.8% of life and terminal illness claims paid, totalling £862.1 million across more than 40,000 claims.

- Royal London, 2024 protection claims, published June 2025: £751 million paid, with 98.7% of all claims accepted.

- Legal & General, 2024: £583 million paid in life claims, supporting more than 14,000 people, as part of over £1 billion in retail protection claims.

- LV=, 2024 claims report: £137 million paid across individual protection, with 95% of all individual protection claims paid.

- Surely analysis of typical UK term life insurance premiums for a healthy applicant, June 2026, including the 20% to 40% variation between insurers for identical cover. Illustrative figures, not quotes.

- Financial Conduct Authority, Pure Protection Market Study, January 2026.

- SunLife, Cost of Dying Report, 2026.

Surely is a trading style of PJG Financial Ltd, authorised and regulated by the Financial Conduct Authority, firm reference number 919697. This page is a financial promotion and is for general information, not personal advice. Life insurance has no cash in value at any time and cover ends if you stop paying premiums. Tax treatment depends on your individual circumstances and may change in the future.