For most people in their 20s, life insurance is not essential, but it can be the smartest time to buy. If no one depends on your income and your only debts would die with you, you can usually wait. If you have a mortgage, a partner who shares the bills, a child, or a debt that someone guaranteed for you, it is worth having now. And because price is driven mostly by age, cover is at its cheapest in your 20s, so locking in a low rate early can save money for decades.

Who needs cover in their 20s, and who can wait

Life insurance pays out money when you die. The honest question is not your age, it is whether anyone would be left worse off financially if your income stopped. That is what decides it.

A quick way to decide

You likely need cover now if

You have bought a home, especially with a partner, since a joint mortgage means your share of the loan would fall on the person you bought with. You have children or anyone who depends on your income. Or you have taken on a debt that someone else guaranteed or holds jointly with you, because that person becomes responsible if you are not there to pay it.

You can usually wait if

You are single, renting, with no children and no one relying on your income, and the only money you owe would be cleared by your estate or written off when you die. In that situation there is often no clear need for cover yet, and there is no harm in waiting until your circumstances change.

Why your 20s are the cheapest time to buy

Age is the single biggest factor in the price of life insurance, ahead of everything except whether you smoke. The younger and healthier you are when you take out a policy, the lower the premium, and on a level term policy that price is fixed for the whole term and never rises.3 Buying in your 20s can lock in a rate that someone starting the same cover in their 40s could not get.

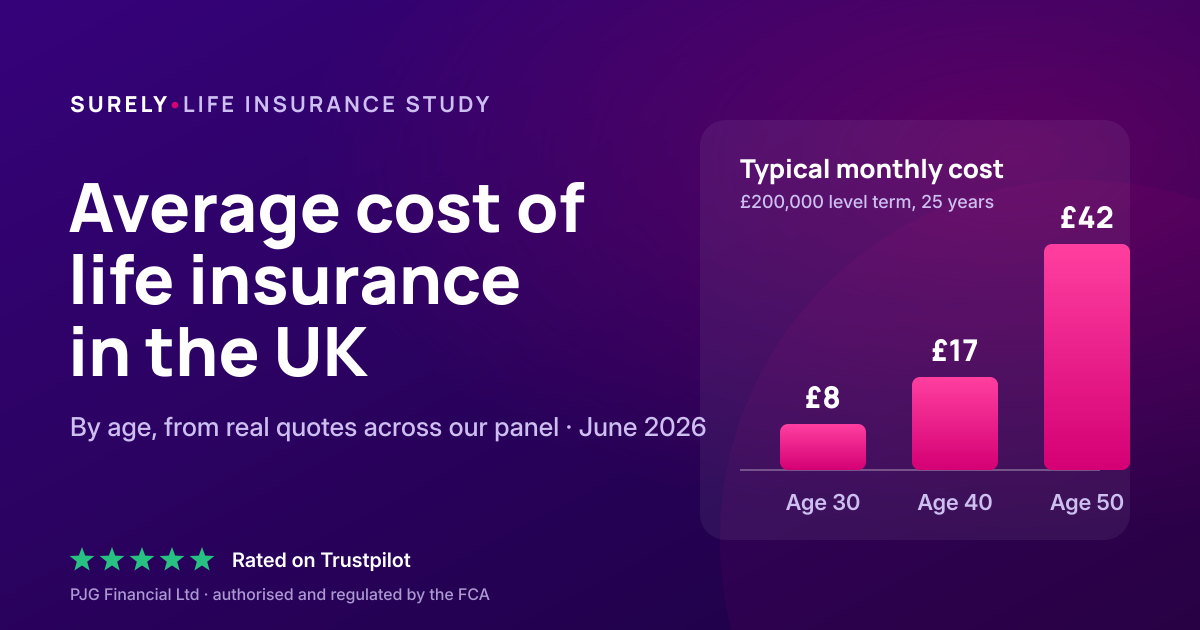

There is a second reason to think about it early. Health can change, and a condition that appears in your 30s can raise your price or limit your options later. Taking cover while you are fit secures both the rate and your eligibility. You can see how price climbs with age in our guide to the average cost of life insurance.

What happens to your debts if you die

A lot of worry in your 20s is about debt, so it helps to be clear about what actually passes to anyone else. Most debts are paid from your estate before anything is inherited, and they are only a reason to buy cover when another person is on the hook for them.

| What you owe | What happens when you die |

|---|---|

| Student loan | Written off in full by the Student Loans Company, and never passed to your family or estate.1 |

| Mortgage | Must be repaid from your estate, or the home may have to be sold, which is why a home is the most common reason to buy cover. |

| Credit cards, overdraft, personal loans | Paid from your estate, not inherited by your family, unless the debt is held jointly. |

| Joint loans or a guarantor | The other person named on the debt becomes responsible for it. |

This is why a student loan on its own is not a reason to take out life insurance. It is cancelled when you die and cannot touch your family.1 A mortgage or a shared debt is a different matter, because it lands on someone you care about.

Do you already have cover through work

Many employers offer death in service, a benefit that pays a lump sum, often a few times your salary, if you die while employed. It is genuinely useful, but it has two limits worth knowing. It usually ends the day you leave that job, so it is not cover you own, and for anyone with a mortgage or a family it may not be enough on its own. Most people treat it as a helpful extra and add their own policy as a top up, rather than relying on it.

How much cover do you need in your 20s

A simple way to size it is to add up the debts that would fall on someone else, chiefly a mortgage, then add a few years of your income if anyone depends on it, and a little for final costs. If you are single with no dependants and no shared debt, you may need very little or none at all. If you have just bought a home with a partner, enough to clear your share of the mortgage is a sensible starting point.

Types of cover that suit your 20s

Most people in their 20s use one of three straightforward options. Level term pays a fixed amount if you die within a set number of years, which suits replacing income or covering an interest only mortgage. Decreasing term falls over time in line with a repayment mortgage, so it is usually the cheapest way to protect a home loan. Family income benefit pays a regular monthly amount instead of a lump sum, which can suit young families who want to replace an income rather than manage a large one off payout.

Common situations in your 20s

If no one relies on your income and your debts would die with you, there is often no clear need for cover yet.

A joint mortgage means your share would fall on your partner. Cover sized to the loan clears it for them.

Children depend on your income, so cover replaces it and protects the home if the worst happens.

There is no death in service to fall back on, and a partner or business may rely on you, so your own cover matters more.

The loan is written off when you die, so it is not a reason on its own. Look at your other commitments instead.

If a home or family is on the horizon, a small policy now locks in a low rate before your price rises with age.

Expert comment

In your 20s the right answer is usually one of two things. Either you have nothing that would land on anyone else, in which case do not let anyone rush you into buying. Or you have just taken on a mortgage or started a family, in which case it is one of the cheapest and most important things you can sort. The trap to avoid is assuming you are too young. Price is set by your age, so the cover only gets more expensive from here.

Paul Gillooly, Founder, Surely

See your own price in minutes

Compare quotes from our panel of UK insurers and find out what cover would cost at your age.

Compare life insurance quotesFrequently asked questions

Do I need life insurance in my 20s?

Not always. If no one relies on your income and your debts would die with you, you can usually wait. You are more likely to need it if you have a mortgage, a partner who shares the bills, children, or a debt that someone guaranteed for you.

Is life insurance cheaper if I get it in my 20s?

Yes. Age is the biggest single driver of price, and a level term premium is fixed for the whole term, so buying young and in good health locks in a low rate that does not rise as you get older.

Do I need life insurance to cover my student loan?

No. UK government student loans are written off in full when you die and never pass to your family or your estate, so a student loan on its own is not a reason to take out cover.

Should I get life insurance if I am single with no children?

Often not yet. With no dependants and no debts that would fall on someone else, you may not need cover. A small policy can still be worth it to lock in a low rate while you are young, or to cover a joint debt or funeral costs.

Do I still need cover if I get death in service through work?

Possibly. Death in service usually pays a few times your salary, but it ends when you leave the job and may not be enough on its own, so people often add their own policy as a top up.

How much life insurance do I need in my 20s?

Enough to clear any debts that would fall on others, chiefly a mortgage, plus a few years of income if anyone depends on you, and a little for final costs. If you are single with no dependants, you may need very little or none.

Sources

- GOV.UK, “Repaying your student loan: when your student loan gets written off or cancelled”. gov.uk

- Financial Conduct Authority, “FCA seeks views on how to help close the protection gap”, January 2026. fca.org.uk

- Surely, “Average cost of life insurance in the UK”. surely.co.uk

Surely is a trading name of PJG Financial Ltd, which is authorised and regulated by the Financial Conduct Authority. FRN 919697.