Is life insurance worth it

It comes down to one thing, whether anyone would struggle financially if you died. If you have a partner, children, a mortgage or other people who rely on your income, it is usually worth it, and cheaper than most people expect. If you are single with no dependants and no debts that pass to others, it often is not.

Get my quoteThe short answer

Life insurance is worth it when your death would leave someone worse off financially. For most people with a family or a mortgage, it is, because the cost is small and the protection is large. For someone single with no dependants and no debts that pass on, it often is not, and that is a perfectly reasonable conclusion.

So the honest question is not whether life insurance is worth it in general. It is whether it is worth it for you. The rest of this guide gives you the case for, the case against, and the numbers to decide.

When it is worth it

Life insurance earns its place when other people depend on your money. If you died, would anyone be left unable to cover the mortgage, the bills or the cost of raising children? If the answer is yes, cover is usually worth it.

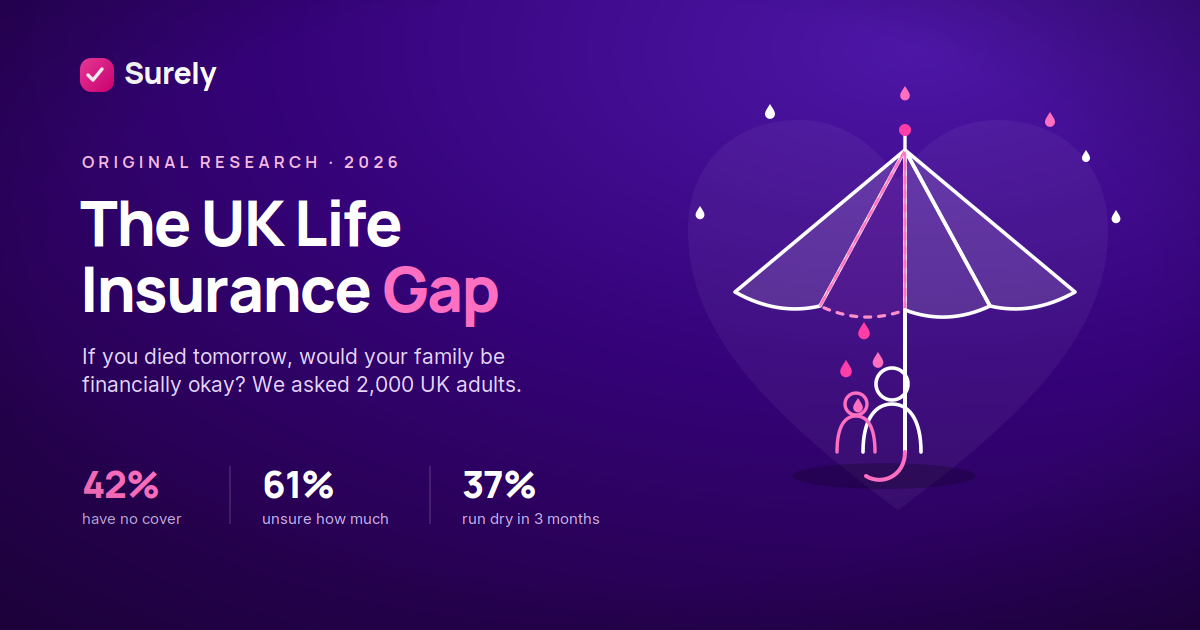

That mainly means people with a family, anyone with a mortgage, and households where one income does most of the heavy lifting. The reason is starker than most people think. Legal and General’s research found the average UK household is only around 19 days from running out of money if its income stops, on median savings of about 2,431 pounds.1 If your income is what keeps the home running, life insurance is the cheap backstop that stops a death becoming a financial crisis. It is worth seeing how long your family could keep the house if your income stopped, and whether your family would be financially okay if the worst happened tomorrow.

When it might not be worth it

It is just as important to say when you can skip it. Cover may not be worth paying for if you are single, have no children or dependants, and no debts that would land on someone else. In that case, your estate is used to settle what you owe, and there is no one left short.

A few other situations call for a closer look rather than an automatic yes.

- You already have enough savings or assets to cover any debts and final costs.

- Your employer’s death in service benefit already covers your needs. Remember it usually ends when you leave the job.

- You are looking at an over 50s plan. These can help with funeral costs, but if you live a long time you may pay in more than the policy pays out, and most have a waiting period in the first year or two.

- If your worry is losing your income to illness rather than death, income protection may fit the need better than life cover.

What you get for the money

For most people who need it, the value case is simple. Cover is cheap next to what it protects. Decreasing term averages about 17 pounds a month and level term about 25 pounds, for 200,000 pounds of cover.2 The average claim actually paid in 2024 was 18,700 pounds, and many policies pay far more.3

Worked example

Pay about 17 pounds a month, roughly 200 pounds a year, for 200,000 pounds of cover. Over a 25 year term that is around 5,000 pounds of premiums to protect a quarter of a million pounds for your family. And the cover does its job: insurers paid 97.9 percent of protection claims, a record 5.32 billion pounds, in 2024.

You can check how much life insurance costs for your own age and situation, but for most healthy adults the monthly price is less than a streaming bundle.

The catch people worry about

The honest objection is this. With term cover, you might pay for years and never claim, because most people outlive their policy. That can feel like wasted money. It is worth being clear about, so here is the fair way to see it.

It is the same deal as home insurance. You pay hoping never to use it, and not claiming means the worst never happened. Term life insurance is protection, not a savings plan, so it builds no cash value and does not pay out if you outlive it. If you want money back at the end you would be looking at a different, far more expensive product, which for most people is not better value. The point of cover is to carry a risk you could not afford to carry yourself, for a price you can.

“I will not tell you everyone needs life insurance, because they do not. If you are single with nothing and no one depending on you, skip it with a clear conscience. But if a partner, a child or a home rests on your income, a few pounds a month buying tens of thousands of pounds of protection is one of the better value things you can do with money. The test is who is left behind, not the product.”

How to make it worth it

If you do need cover, a few choices decide whether it is good value or not.

- Buy it sooner. Premiums rise with age and health changes, so the younger and healthier you are, the cheaper it locks in.

- Match the type and amount to the need, so you are not paying for cover you will not use, or leaving a gap.

- Consider writing it in trust, which can speed the payout to your family and keep it outside your estate for inheritance tax.

- Answer the health questions honestly, so the policy actually pays when it is needed.

- Compare insurers for the same cover, because prices for an identical policy vary.

Common questions

Is life insurance worth it if I am single?

Usually not, unless you have debts someone else would inherit, such as a joint loan, or you want to leave money for a funeral or a gift. With no dependants and no shared debts, there is often no one left worse off.

Is it worth it if I have no children?

It depends on whether a partner relies on your income or shares your mortgage. If losing your income would leave them struggling, cover is still worth considering. If not, it may not be needed.

Is it a waste of money if I never claim?

No more than home insurance you never claim on. Most term policies do not pay out because the person outlives them, which is the good outcome. You are buying protection against a risk you could not otherwise afford, not a savings pot.

Is over 50s life insurance worth it?

It can help cover a funeral and leave a small sum, with no medical questions. The trade off is that if you live a long time you may pay in more than it pays out, and there is usually a waiting period in the first year or two. Weigh the likely premiums against the payout.

Is it better to just save instead?

They do different jobs. Savings take years to build, while cover protects the full amount from day one. With the average household around 19 days from the breadline, savings alone rarely fill the gap that a death would leave.

When is the best time to get it?

Generally as soon as someone depends on you, because cover is cheaper the younger and healthier you are. Waiting usually means paying more for the same protection.

Is it worth it, in numbers

A summary of the figures behind this guide.

| The picture in numbers | Figure |

|---|---|

| Days the average household is from the breadline | About 19 |

| Average household savings | £2,431 |

| Adults who hold life insurance | 28% |

| Typical cost to protect a mortgage | About £17 a month |

| Average individual claim paid | £18,700 |

| Protection claims paid | 97.9% or more for a decade |

Surely analysis of Legal and General Deadline to Breadline research, FCA Financial Lives 2024, myTribe 2026 pricing and ABI protection claims 2024.1423

Not sure if it stacks up for you? See your price in a couple of minutes

Get my quoteDeciding what is right for you

Strip away the sales talk and it comes to one question. If you died tomorrow, would someone you care about be left financially worse off? If yes, life insurance is almost always worth the small monthly cost, and worth buying sooner rather than later. If no, you can pass on it without guilt. Work out who depends on you, get the right type and amount, and compare a few insurers so the cover is as good value as it is useful.

Found that it is worth it for you? Compare cover now

Get my quoteWhether cover is right for you depends on your personal circumstances. Cover, price and eligibility depend on your age, health, occupation and smoker status, and on insurer terms. Tax treatment depends on your circumstances and can change. Surely is operated by PJG Financial Ltd, which is authorised and regulated by the Financial Conduct Authority, FRN 919697.

How we researched this guide

We write our guides from named, public UK sources and cross check the figures rather than rely on a single site. Where we say “Surely analysis”, it means we have compiled and compared published data, not produced the raw figures ourselves.

The data on this page draws on:

- Legal and General, Deadline to Breadline research, for how long households could cope without income.

- myTribe Life Insurance Pricing Survey 2026, for average monthly premiums.

- Association of British Insurers and GRiD, protection claims data 2024, for claims paid and the average claim.

- FCA Financial Lives 2024, for the share of adults holding life insurance.

Cost figures are illustrative averages, not quotes. Whether cover is worth it depends on your own circumstances.

Surely compares cover from a selected panel of UK insurers and protection providers, not the whole of the market. Surely may receive a commission from the provider you take out cover with, which does not affect the price you pay.

Written and reviewed by Paul Gillooly, Founder of Surely. Last reviewed June 2026.

Sources

- Legal and General, Deadline to Breadline research. Average UK household around 19 days from running out of money if income stops, on median savings of about £2,431. legalandgeneral.com

- myTribe Life Insurance Pricing Survey 2026. Average monthly premiums: decreasing term £16.58, level term £25.05, over 50s £29.45.

- Association of British Insurers and GRiD, protection claims data 2024, published July 2025. 97.9% of individual claims paid over the past decade; £5.32 billion individual protection; average individual claim £18,700. abi.org.uk

- Financial Conduct Authority, Financial Lives 2024 survey. 28% of adults held life insurance, with above average declines among mortgage holders. fca.org.uk